Fill Your Ma Exempt St 12 Form

Fill Your Ma Exempt St 12 Form

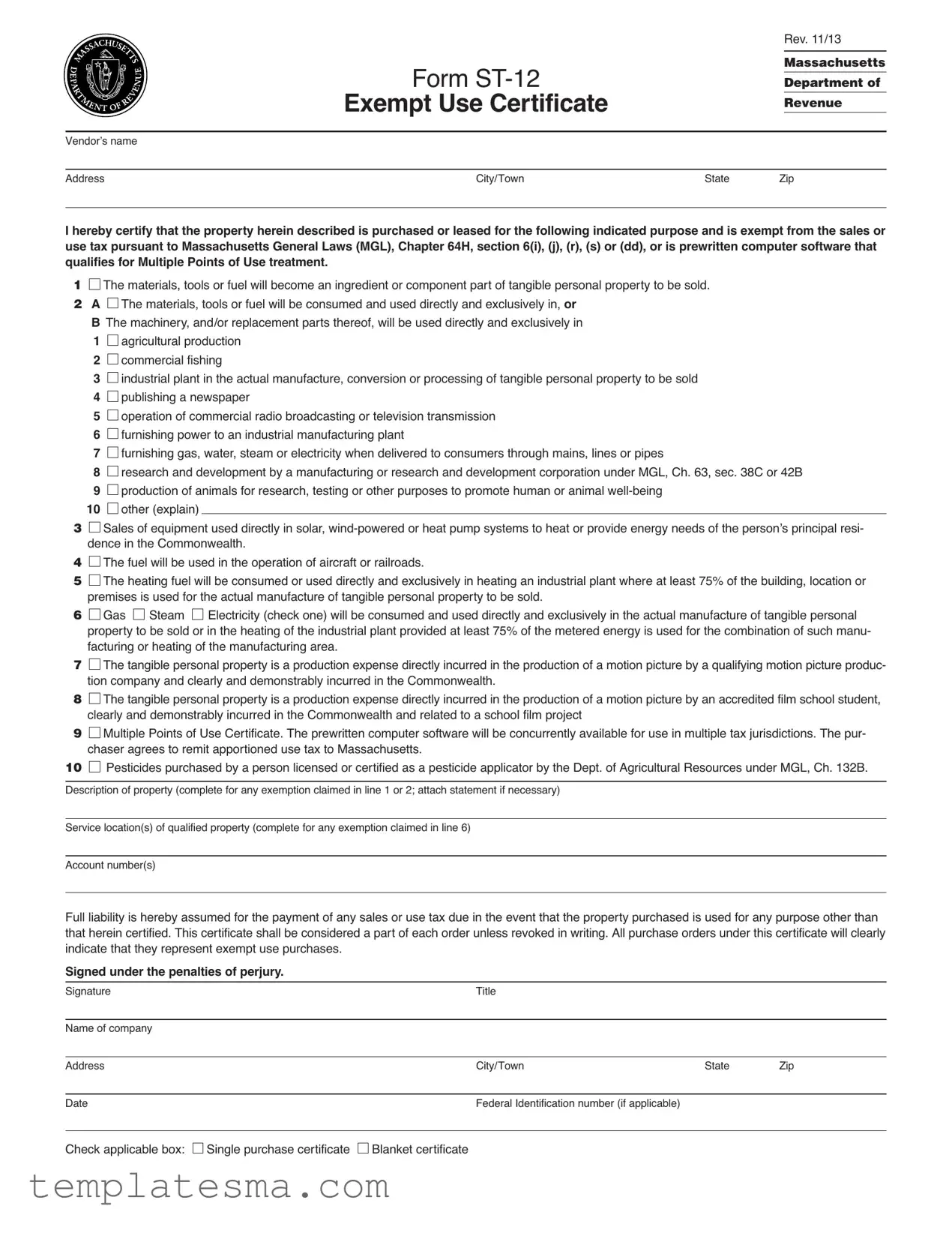

In Massachusetts, businesses and individuals engaging in specific activities may be eligible for sales or use tax exemptions under certain conditions. The Form ST-12 Exempt Use Certificate, revised in November 2013, serves as a critical tool for these entities to certify the exemption status of their purchases or leases, according to the Massachusetts Department of Revenue. This comprehensive document outlines a variety of exempt purposes, such as purchases that directly contribute to agricultural production, commercial fishing, manufacturing, publishing, broadcasting, and more. For instance, materials that will become an integral part of tangible personal property for sale, machinery used in specific sectors, and energy for industrial plants are among the items that can qualify for exemptions. Furthermore, the form addresses the exemption for prewritten computer software used in multiple jurisdictions and for pesticides by certified applicators. Vendors and purchasers must ensure that the form is properly completed and retained to meet legal requirements, as it relieves vendors of the burden of proving the exempt status of sales when accepted in good faith. Additionally, the form provides specific instructions for contractors, cautioning about their responsibility to prove exemptions and their potential liability for taxes if the purchased items do not qualify. The significance of Form ST-12 extends beyond the immediate financial benefit of tax exemptions, emphasizing the importance of understanding and complying with Massachusetts tax laws to avoid penalties for misuse. For detailed guidance, including the exceptions and specific uses not covered by Form ST-12, the Massachusetts Department of Revenue remains a pivotal resource.

Form

Exempt Use Certificate

Rev. 11/13

Massachusetts

Department of

Revenue

Vendor’s name

Address |

City/Town |

State |

Zip |

I hereby certify that the property herein described is purchased or leased for the following indicated purpose and is exempt from the sales or use tax pursuant to Massachusetts General Laws (MGL), Chapter 64H, section 6(i), (j), (r), (s) or (dd), or is prewritten computer software that qualifies for Multiple Points of Use treatment.

1 The materials, tools or fuel will become an ingredient or component part of tangible personal property to be sold.

The materials, tools or fuel will become an ingredient or component part of tangible personal property to be sold.

2A  The materials, tools or fuel will be consumed and used directly and exclusively in, or B The machinery, and/or replacement parts thereof, will be used directly and exclusively in 1

The materials, tools or fuel will be consumed and used directly and exclusively in, or B The machinery, and/or replacement parts thereof, will be used directly and exclusively in 1  agricultural production

agricultural production

2  commercial fishing

commercial fishing

3  industrial plant in the actual manufacture, conversion or processing of tangible personal property to be sold 4

industrial plant in the actual manufacture, conversion or processing of tangible personal property to be sold 4  publishing a newspaper

publishing a newspaper

5 operation of commercial radio broadcasting or television transmission

operation of commercial radio broadcasting or television transmission

6 furnishing power to an industrial manufacturing plant

furnishing power to an industrial manufacturing plant

7 furnishing gas, water, steam or electricity when delivered to consumers through mains, lines or pipes

furnishing gas, water, steam or electricity when delivered to consumers through mains, lines or pipes

8 research and development by a manufacturing or research and development corporation under MGL, Ch. 63, sec. 38C or 42B

research and development by a manufacturing or research and development corporation under MGL, Ch. 63, sec. 38C or 42B

9 production of animals for research, testing or other purposes to promote human or animal

production of animals for research, testing or other purposes to promote human or animal

10 other (explain)

other (explain)

3 Sales of equipment used directly in solar,

Sales of equipment used directly in solar,

4 The fuel will be used in the operation of aircraft or railroads.

The fuel will be used in the operation of aircraft or railroads.

5 The heating fuel will be consumed or used directly and exclusively in heating an industrial plant where at least 75% of the building, location or premises is used for the actual manufacture of tangible personal property to be sold.

The heating fuel will be consumed or used directly and exclusively in heating an industrial plant where at least 75% of the building, location or premises is used for the actual manufacture of tangible personal property to be sold.

6 Gas

Gas  Steam

Steam  Electricity (check one) will be consumed and used directly and exclusively in the actual manufacture of tangible personal property to be sold or in the heating of the industrial plant provided at least 75% of the metered energy is used for the combination of such manu- facturing or heating of the manufacturing area.

Electricity (check one) will be consumed and used directly and exclusively in the actual manufacture of tangible personal property to be sold or in the heating of the industrial plant provided at least 75% of the metered energy is used for the combination of such manu- facturing or heating of the manufacturing area.

7 The tangible personal property is a production expense directly incurred in the production of a motion picture by a qualifying motion picture produc- tion company and clearly and demonstrably incurred in the Commonwealth.

The tangible personal property is a production expense directly incurred in the production of a motion picture by a qualifying motion picture produc- tion company and clearly and demonstrably incurred in the Commonwealth.

8 The tangible personal property is a production expense directly incurred in the production of a motion picture by an accredited film school student, clearly and demonstrably incurred in the Commonwealth and related to a school film project

The tangible personal property is a production expense directly incurred in the production of a motion picture by an accredited film school student, clearly and demonstrably incurred in the Commonwealth and related to a school film project

9 Multiple Points of Use Certificate. The prewritten computer software will be concurrently available for use in multiple tax jurisdictions. The pur- chaser agrees to remit apportioned use tax to Massachusetts.

Multiple Points of Use Certificate. The prewritten computer software will be concurrently available for use in multiple tax jurisdictions. The pur- chaser agrees to remit apportioned use tax to Massachusetts.

10 Pesticides purchased by a person licensed or certified as a pesticide applicator by the Dept. of Agricultural Resources under MGL, Ch. 132B.

Pesticides purchased by a person licensed or certified as a pesticide applicator by the Dept. of Agricultural Resources under MGL, Ch. 132B.

Description of property (complete for any exemption claimed in line 1 or 2; attach statement if necessary)

Service location(s) of qualified property (complete for any exemption claimed in line 6)

Account number(s)

Full liability is hereby assumed for the payment of any sales or use tax due in the event that the property purchased is used for any purpose other than that herein certified. This certificate shall be considered a part of each order unless revoked in writing. All purchase orders under this certificate will clearly indicate that they represent exempt use purchases.

Signed under the penalties of perjury.

Signature |

Title |

|

|

|

|

|

|

Name of company |

|

|

|

|

|

|

|

Address |

City/Town |

State |

Zip |

|

|

|

|

Date |

Federal Identification number (if applicable) |

|

|

Check applicable box:

Single purchase certificate

Single purchase certificate

Blanket certificate

Blanket certificate

Form

General Information

Certain consumers may not be required to pay a sales tax if the property they purchase is to be used in a manner which exempts it from taxation.

If tangible personal property, including fuel, gas, steam or electric- ity is purchased and that purchase qualifies for an exemption from the sales or use tax, the purchaser may present an exempt use certificate to the vendor to certify that the property will be used in an exempt manner. The burden of proving that a sale of tangible personal property by any vendor is exempt from tax is on the ven- dor, unless the vendor accepts from the purchaser a certificate declaring that the property is exempt from tax. The Multiple Points of Use Certificate claimed on line 9 is only applicable to prewritten computer software that will be concurrently available for use in multiple tax jurisdictions.

Notice to Vendors

The vendor must make sure that the certificate is completed prop- erly and signed before accepting it.

An exempt use certificate relieves the vendor from the burden of proof only if it is taken in good faith from a purchaser who, at the time of purchase, intends to use the property in an exempt man- ner, or is unable to ascertain at the time of purchase that it will be used in an exempt manner.

A Multiple Points of Use Certificate claimed on line 9 relieves the vendor from the obligation to collect, pay, or remit the applicable tax on sales of prewritten software.

The exemption claimed on line 10 for sales to a person licensed or certified as a pesticide applicator by the Department of Agricultural Resources under MGL, Ch. 132B only applies to sales of pesticides, including insecticides, herbicides, fungicides, miticides and all mate- rials registered with the Environmental Protection Agency as pesti- cides under Federal Insecticide, Fungicide and Rodenticide Act as well as other pesticides commonly regarded in the same category and for the same purpose. See TIR

The vendor must retain this certificate as part of his/her tax rec- ords. For further information regarding the requirements for retain- ing records, see Massachusetts Regulation, 830 CMR 62C.25.1.

Notice to Contractors

This form may be used by a contractor when purchasing or leasing tangible personal property from a vendor in connection with fulfilling a contract with its customer if the property will be used for one of the exempt uses described in Massachusetts General Laws (MGL) chapter 64H, section 6(r) or (s), which include the following: use di- rectly and exclusively in an industrial plant in the actual manufac- ture of tangible personal property to be sold; in the furnishing of power to an industrial manufacturing plant; in the furnishing of gas, water, steam or electricity when delivered to consumers through mains, lines or pipes; in research and development by a manufac- turing corporation or research and development corporation; in ag- ricultural production; in commercial fishing.

A contractor purchasing property exempt under MGL chapter 64H, section 6(r) or (s), may sign and present this form to its vendor. The contractor bears the burden of proof of demonstrating on audit that the items purchased are or will be used in an exempt manner. In the event that the items do not qualify for exemption under section 6(r) or (s), the contractor will be liable for the tax. An exempt use cer- tificate furnished by the contractor’s customer to the contractor will not relieve the contractor from liability. See DD

Notice to Purchasers

This form is not to be used by an exempt organization (use Form

If a purchaser makes any use of the property other than an exempt use, such property will be subject to the Massachusetts sales or use tax, as of the time the property is first used.

For any exemption claimed in line 1 or 2, the purchaser must pro- vide a description of the exempt property. For any exemption claimed in line 6 for the purchase of gas, steam or electricity, the purchaser must provide the service locations of the qualified prop- erty and utility account numbers. Attach an additional statement if more space is needed.

A purchaser submitting a Multiple Points of Use Certificate by checking line 9 agrees to report and remit the applicable sales or use tax to the jurisdictions where the software will be used, using any reasonable, but consistent and uniform, method of apportion- ment that is supported by the purchaser’s business records, as they exist at the time a return is filed. See TIR

If at any time a business that has presented this certificate ceases to qualify for the exemption, it must revoke in writing the Form ST- 12 it has given to its vendor(s).

For further information regarding the acceptance or use of exempt use certificates see Massachusetts Regulation, 830 CMR 64H.8.1.

Warning: Willful misuse of this certificate may result in crimi- nal tax evasion penalties of up to one year in prison and $10,000 ($50,000 for corporations) in fines.

If you have any questions about the acceptance or use of this cer- tificate, please contact: Massachusetts Department of Revenue,

Customer Service Bureau, PO Box 7010, Boston, MA 02204; (617)

printed on recycled paper

printed on recycled paper

| Fact | Detail |

|---|---|

| Form Name | ST-12 Exempt Use Certificate |

| Revision Date | November 2013 |

| Issuing Agency | Massachusetts Department of Revenue |

| Purpose | Allows purchasers to certify their purchase is for an exempt use, exempting it from sales or use tax |

| Governing Law | Massachusetts General Laws (MGL), Chapter 64H, sections 6(i), (j), (r), (s), or (dd) |

| Applicability | Used for purchases or leases of property, including prewritten computer software for Multiple Points of Use, intended for exempt uses |

| Responsibilities of the Vendor | Ensure the certificate is completed and signed; retain the certificate as part of tax records |

| Exemptions Described | Includes materials for manufacturing, agricultural production, commercial fishing, and more |

| Warning | Willful misuse may result in criminal tax evasion penalties, including fines and imprisonment |

| Contact Information | Massachusetts Department of Revenue, Customer Service Bureau, PO Box 7010, Boston, MA 02204; (617) 887-MDOR or toll-free in-state 1-800-392-6089 |

| Special Notes | The form cannot be used by exempt organizations, for off-premises food containers, or to claim the small business energy exemption |

Before diving into the details of the Massachusetts Exempt Use Certificate, Form ST-12, it's essential to grasp its purpose. This form plays a critical role for eligible individuals or businesses that make purchases exempt from sales tax. Ensuring that every section is filled out accurately is key to leveraging these exemptions. Below is a straightforward guide to help navigate the form.

Upon completing Form ST-12, it's crucial to present this certificate to the vendor prior to making your purchase to ensure the transaction is processed as tax-exempt. Keep a copy for your records alongside any relevant purchase documentation. Remaining diligent in documenting exempt transactions will streamline any future validation processes required by the Massachusetts Department of Revenue.

What is the purpose of Form ST-12 Exempt Use Certificate?

The Form ST-12 Exempt Use Certificate is designed for purchasers in Massachusetts to certify that the property they are buying or leasing is for a specific use that exempts it from sales or use tax according to Massachusetts General Laws (MGL), Chapter 64H, section 6. This includes materials, tools, fuel, and some machinery and replacement parts used in agricultural production, commercial fishing, manufacturing, and other specified exempt activities. Additionally, it covers prewritten computer software under the Multiple Points of Use treatment, and certain sales of equipment used in solar, wind-powered, or heat pump systems for residential energy needs.

Who is eligible to use Form ST-12?

Eligibility to use Form ST-12 includes individuals or businesses purchasing or leasing tangible personal property or services that will be used in a manner qualifying for exemption from sales or use tax under specified sections of the Massachusetts General Laws. This includes entities engaged in manufacturing, agricultural production, commercial fishing, publishing, broadcasting, research and development, and similar activities. Contractors performing eligible projects may also use this form as specified under the law.

How does presenting Form ST-12 affect a vendor?

When a purchaser presents a fully completed and signed Form ST-12, the burden of proof for the sale being exempt from sales or use tax shifts from the vendor to the purchaser. The vendor must retain this certificate as part of their tax records but is relieved from the obligation of proving the tax-exempt nature of the sale at the time of audit, assuming the certificate was accepted in good faith based on the purchaser's intent.

Can Form ST-12 be used for multiple purchases?

Yes, Form ST-12 can serve as either a single purchase certificate or a blanket certificate for ongoing exempt purchases. The appropriate box must be checked to indicate the intended use. If used as a blanket certificate, all future purchases that meet the exemption criteria do not require a new form, unless the terms of the exemption change or the certificate is revoked in writing.

What are the consequences of misusing Form ST-12?

Intentional misuse of the Form ST-12 Exempt Use Certificate, such as claiming an exemption for which the purchaser or the purchased property is not eligible, may lead to criminal tax evasion charges. Consequences can include imprisonment for up to one year and fines up to $10,000 for individuals or $50,000 for corporations. Therefore, it is crucial to ensure that all the criteria for tax exemption are met and the form is used correctly.

What should a purchaser do if their exemption status changes?

If a purchaser’s exemption status changes, meaning the property purchased under the exemption is no longer being used in an exempt manner, the purchaser is required to notify their vendor(s) by revoking the Form ST-12 in writing. Additionally, the purchaser must begin to pay sales or use tax for the property from the time it is first used in a non-exempt manner.

When completing the Massachusetts Exempt Use Certificate (Form ST-12), individuals and businesses often make errors that can lead to complications or misunderstandings with tax regulations. Avoiding these mistakes ensures compliance with Massachusetts tax laws and can prevent unnecessary penalties. Here are five common errors:

Not specifying the exact exemption reason: The form allows for various exemptions under Massachusetts General Laws, Chapter 64H, section 6. Many people forget to clearly indicate which specific exemption(s) apply to their purchase. It’s crucial to identify whether the property is purchased for agriculture, industrial manufacturing, research and development, or another qualified exemption reason, and explicitly state this on the form.

Incomplete description of property: For any exemption claimed, particularly those under line 1 or 2, the form requires a detailed description of the exempt property. A common mistake is providing vague or incomplete descriptions, making it difficult for the Massachusetts Department of Revenue to ascertain the property’s eligibility for tax exemption. Detailed descriptions support the legitimacy of the exemption claim.

Failing to provide service locations or account numbers: When claiming an exemption for utilities such as gas, steam, or electricity under line 6, it's mandatory to list the service locations and utility account numbers. This information is often overlooked, leading to a rejection of the exemption claim because the Department cannot verify the proper use of the utility services in relation to the exemption criteria.

Improper use of the certificate for ineligible entities: The ST-12 form is not applicable to exempt organizations, which should use Form ST-5, nor is it for claiming exemptions for food or drink containers or small business energy exemptions. Yet, entities mistakenly use this form for those purposes. Recognizing the correct form for specific exemptions is essential for compliance and valid exemption claims.

Incorrectly applying the Multiple Points of Use (MPU) Certificate: The MPU exemption, noted on line 9, is solely for prewritten computer software used in multiple tax jurisdictions. A frequent mistake is misapplying this exemption to other types of property or not agreeing to remit apportioned use tax to Massachusetts. It's critical to understand and respect the narrow scope of this exemption to prevent misuse.

By addressing these frequent mistakes, purchasers can accurately complete the Massachusetts Exempt Use Certificate (Form ST-12), ensuring that their tax-exempt transactions are both valid and verifiable by the Massachusetts Department of Revenue.

When dealing with the Massachusetts Exempt Use Certificate (Form ST-12), it's essential to be aware of the other forms and documents that you might need, depending on your specific situation. Understanding these additional forms can help you ensure full compliance with Massachusetts tax laws and avoid any potential misunderstanding or misuse of the exemption.

Each of these documents has its unique purpose and requirements. By familiarizing yourself with these forms, you can navigate the specifics of Massachusetts sales and use tax more effectively. Remember, proper documentation and adherence to the guidelines for each form are vital to maintaining compliance and leveraging tax exemptions correctly for your business or organization.

The Ma Exempt St 12 form is similar to other tax exemption documents that serve to declare the intended exempt use of purchased goods or services, aiming to ensure that only the eligible purchases avoid the usual sales or use taxes. These documents generally share the objective of providing proof to vendors and tax authorities that the purchase qualifies under specific legal exemptions, thus avoiding the sales tax. Each document, including the Ma Exempt St 12 form, contains detailed instructions for both the purchaser and the vendor, emphasizing the conditions under which the exemption is claimed, the types of purchases that qualify, and the responsibilities of both parties to comply with the state tax laws.

Form ST-5, Exempt Purchaser Certificate, is remarkably similar to the Ma Exempt St 12 form in that it is used to certify that a purchase is tax-exempt. However, the ST-5 form is specifically tailored for use by tax-exempt organizations, such as non-profits. Both forms require the purchaser to provide a detailed explanation of how the purchased goods or services qualify for the exemption. The critical difference lies in the eligibility criteria: while the ST-12 form focuses on the use of goods in specific exempt activities such as manufacturing or research, the ST-5 hones in on the purchaser's exempt status as a non-profit organization under Massachusetts law.

Form ST-12EC, Exempt Use Certificate for Containers, is another document whose purpose aligns closely with that of the Ma Exempt St 12 form, focusing instead on the exemption for containers used in the transport of food or drink. Like the ST-12 form, the ST-12EC also necessitates the purchaser's certification that the use of the purchased items aligns with the conditions for tax exemption stipulated by Massachusetts law. Though both cater to different niches—ST-12 for a broad range of goods and ST-12EC specifically for containers—each document plays a crucial role in clarifying the nature of tax-exempt purchases and safeguarding against misuse of the exemption.

Form ST-13, Small Business Energy Exemption Certificate, shares similarities with the Ma Exempt St 12 form in its purpose to exempt eligible purchases from sales and use taxes. The ST-13 form, specifically dedicated to small businesses claiming exemptions on energy purchases, mirrors the ST-12 form's requirement for the purchaser to assert the purpose and eligibility of the exemption. While the Ma Exempt St 12 form encompasses a broader range of exemptions, including but not limited to energy, the ST-13 zeroes in on providing relief to small businesses on their energy consumption costs, highlighting the targeted approach of tax exemption documents to cater to specific sectors or types of purchases.

When filling out the Massachusetts Exempt Use Certificate (Form ST-12), there are several key steps and precautions to take to ensure the form is completed accurately and in compliance with state regulations. Below is a list of do's and don'ts to guide you through the process.

Do:By following these guidelines, you will help ensure the process goes smoothly and that your Form ST-12 is processed efficiently and effectively.

Understanding the Massachusetts Form ST-12 Exempt Use Certificate can be tricky. Here are six common misconceptions clarified for better comprehension:

This is incorrect. Form ST-12 is specific to exempting purchases from sales and use tax under certain conditions outlined by Massachusetts General Laws, primarily for manufacturing, agricultural, commercial fishing, and other specified operational needs. Other forms, like the ST-5 for exempt organizations or the ST-13 for small business energy exemptions, are necessary for their respective purposes.

Not all businesses qualify for the exemptions listed on Form ST-12. Only those engaged in specific activities, such as agricultural production, commercial fishing, industrial manufacturing, or related sectors, which meet the exemptions criteria, can utilize this form. Understanding the eligibility requirements is crucial.

Merely submitting the Form ST-12 does not grant the exemption. The purchaser must correctly complete and provide the form to the vendor, specifying the exemption reason. The vendor is responsible for ensuring the form is properly completed and maintaining it as part of their sales tax records.

Form ST-12 does not blanket all purchases a company makes. The form is used to certify that specific purchased or leased items are for exempt uses as outlined by Massachusetts law. Each qualifying purchase category might require additional documentation or specific details on how the exemption applies.

While primarily focused on goods such as tangible personal property and specific utilities, Form ST-12 also applies to certain services related to exempt uses, such as production expenses for motion pictures. It's important to carefully review the form's criteria and applicable laws to determine eligibility.

The exemption for utilities like gas, steam, and electricity require that they be used directly and exclusively in manufacturing or in heating the manufacturing area while meeting certain percentage usage criteria. Simply buying these utilities does not guarantee the exemption; their use must align with the requirements stated in the law.

When in doubt, consulting the Massachusetts Department of Revenue or a tax professional can clarify these exemptions and ensure proper compliance with state laws.

When dealing with the Massachusetts Exempt Use Certificate (Form ST-12), several crucial points need to be understood by both vendors and purchasers to ensure compliance with the state's tax laws. Understanding these key takeaways can help prevent misuse of the certificate and ensure transactions are processed correctly.

Accordingly, both vendors and purchasers must be diligent in their understanding and use of Form ST-12 to ensure compliance with Massachusetts tax laws, thereby avoiding any legal or financial repercussions.

Cd Copy Order Massachusetts - The document is a testament to the legal field's adaptation of technology, offering a streamlined approach to accessing court recordings.

M-941 - Emphasizes the importance of providing a business name and address for identification purposes.

Ma Form Abt - A power of attorney section enables taxpayers to appoint representatives to handle their abatement requests.