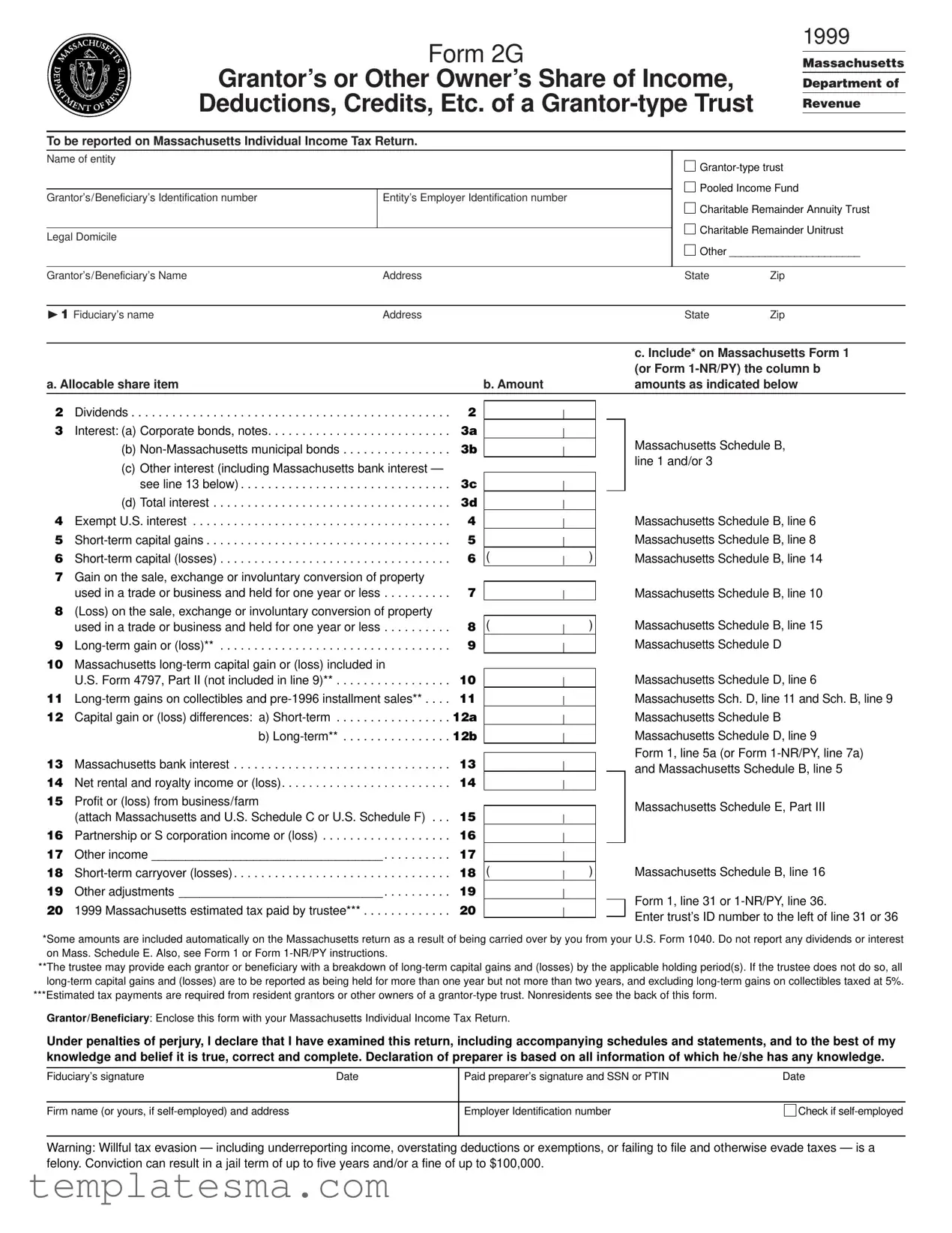

What is the Massachusetts Form 2G?

Form 2G, also known as Grantor’s or Other Owner’s Share of Income, Deductions, Credits, Etc. of a Grantor-type Trust, is a document required by the Massachusetts Department of Revenue. It's used by grantors or other owners of a grantor-type trust to report their share of income, deductions, and credits to the state for tax purposes.

Who needs to file Form 2G in Massachusetts?

Any grantor or other owner of a grantor-type trust must file Form 2G if they receive income, deductions, or credits that must be reported on their Massachusetts Individual Income Tax Return.

What types of trusts require the filing of Form 2G?

Form 2G must be filed for grantor-type trusts. This includes pooled income funds, charitable remainder annuity trusts, charitable remainder unitrusts, and other similar legal arrangements where the income is either distributed to or accumulated for the benefit of the grantor or the grantor's spouse.

How do I report dividends and interest from my grantor-type trust on my Massachusetts tax return?

Dividends and interests should be reported on Massachusetts Form 1 (or Form 1-NR/PY) using the amounts from Form 2G. Dividends are entered as part of the "Dividends" line, while interest is broken down into different categories, such as corporate bonds and bank interest, and reported accordingly on the Massachusetts Schedule B.

Are there any specific instructions for non-residents with a Massachusetts source income from a grantor-type trust?

Yes, non-residents with Massachusetts source income from a grantor-type trust must have income tax withheld by the trustee at the applicable rates. This amount is then reported on their income tax return. Non-residents should review the details on the back of Form 2G for specific instructions.

What do I do if I have long-term capital gains or losses?

If you have long-term capital gains or losses from a grantor-type trust, the trustee is expected to provide a breakdown by the holding period. This information is then reported on the Massachusetts Schedule D, following the instructions provided on Form 2G.

Is there a provision for estimated tax payments?

Yes, estimated tax payments are required for resident grantors or other owners of a grantor-type trust. Form 2G includes a section for reporting these estimated tax payments made by the trustee on behalf of the grantor or owner.

Can I file for an extension if I cannot complete Form 2G by the due date?

Yes, you can file an Application for Extension of Time to File using Form M-8736. This extension applies to the filing deadline and not to any payment due. An extension can give you up to six additional months to file.

What are the filing options if I need to file more than one Form 2G?

If you are required to file multiple Forms 2G, you can file them on a consolidated basis. A single Form 2, labeled as a "Consolidated Form 2G," serves as the cover for all attached Forms 2G. Detailed instructions for consolidated filing are provided in the Form 2G instructions.

When is Form 2G due, and where should it be mailed?

Form 2G is generally due on April 18, 2000, for the tax year 1999. If you are filing on a fiscal year basis, the form is due by the 15th day of the fourth month after the end of the fiscal year. Completed forms should be mailed to the Massachusetts Department of Revenue, PO Box 7017, Boston, MA 02204. For any inquiries, not related to the returns themselves, you can contact the Massachusetts Department of Revenue's Customer Service Bureau.