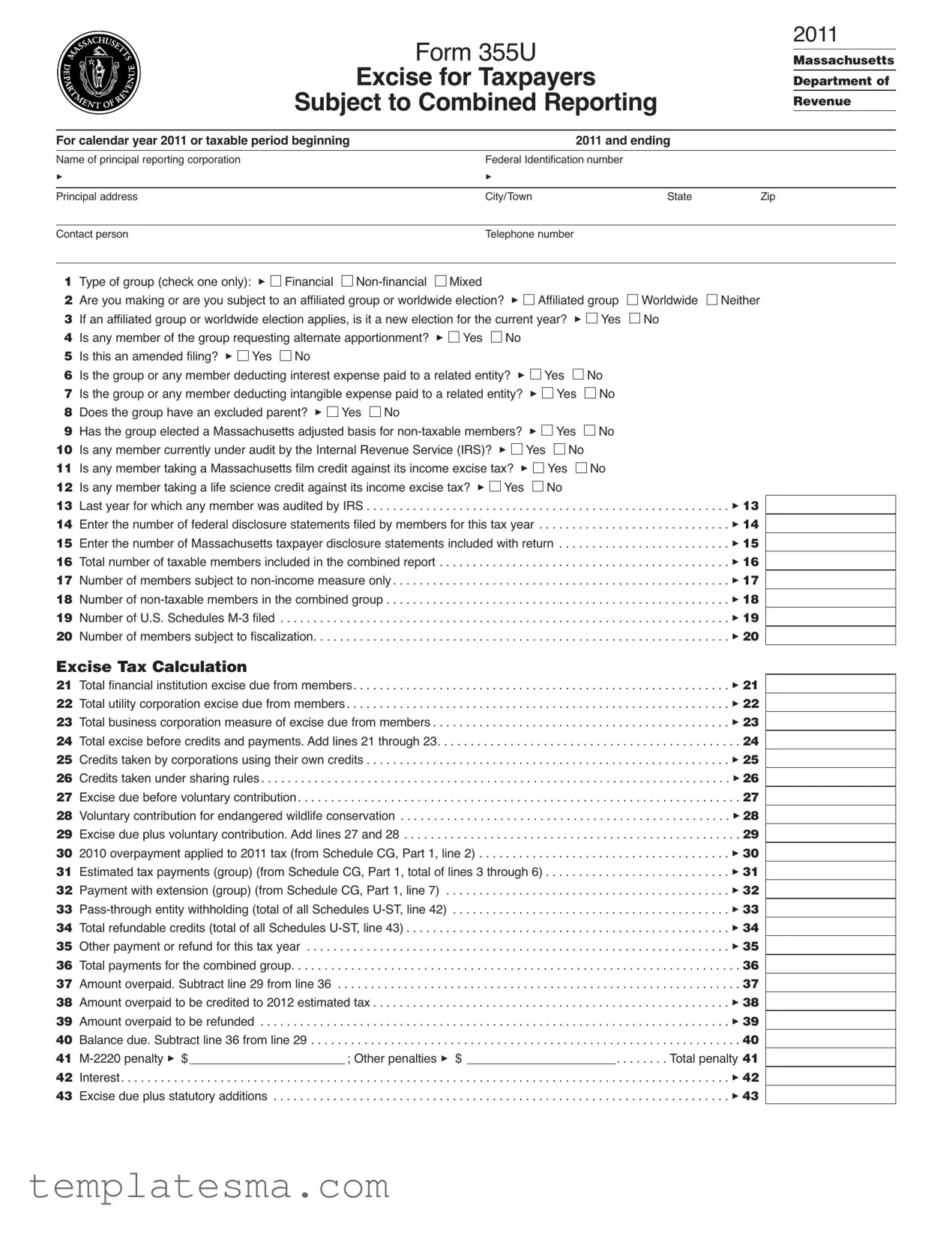

What is the Form 355U in Massachusetts?

Form 355U is an excise tax form used by taxpayers in Massachusetts that are subject to combined reporting. This includes groups of corporations that combine their incomes for tax purposes. The form is used to report income, calculate excise tax due, and claim any relevant credits for the fiscal calendar year 2011 or for a taxable period that begins in 2011 and ends afterward.

Who needs to file Form 355U?

Any corporate group operating in Massachusetts that is required to file taxes using combined reporting must file Form 355U. This includes groups that consist of financial, non-financial, and mixed corporations. The principal reporting corporation, responsible for the combined report, files this form on behalf of the group.

What information is required to complete Form 355U?

To complete Form 355U, the principal reporting corporation must provide its name, federal identification number, principal address, and contact information. Additionally, the form requires details about the type of group (financial, non-financial, or mixed), any elections made regarding affiliated groups or worldwide income, alternative apportionment requests, and whether the filing is an amendment. Information on deductions for interest and intangible expenses paid to related entities, audit statuses, and various credit claims is also required.

How do you determine if your group is subject to combined reporting?

In Massachusetts, a group of corporations is subject to combined reporting if the members are engaged in a unitary business, with more than 50% of voting control of each member corporation directly or indirectly held by a common owner. The idea is to tax corporations based on their combined business activities in the state, rather than on an individual basis. If your corporate group operates together in a cohesive manner that contributes to the generation of income through shared or interdependent activities, you are likely subject to combined reporting.

Can you amend Form 355U after it has been filed?

Yes, if there are changes to the information previously reported or if errors are found on the original Form 355U submitted, the principal reporting corporation can file an amended Form 355U. This involves checking the "Yes" box for question 5 on the form, indicating that the submission is an amendment, and providing the corrected information.

What are the deadlines for filing Form 355U?

The deadline for filing Form 355U typically aligns with the federal income tax return deadline for corporations, which is the 15th day of the fourth month following the end of the corporation's tax year. For corporations that operate on a calendar-year basis, the deadline would be April 15th of the following year. If the due date falls on a weekend or holiday, the deadline is extended to the next business day.

Where can you find Form 355U and its instructions?

Form 355U and its detailed instructions can be found on the Massachusetts Department of Revenue's website. The website provides access to current and prior year forms, along with instructions that include definitions, filing requirements, and guidance on how to calculate the tax and credits. Taxpayers can download the form directly from the site to complete and file with the state.

Financial

Financial

Mixed

Mixed

Affiliated group

Affiliated group

Worldwide

Worldwide

Neither

Neither

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No

Yes

Yes

No

No Yes

Yes  No

No Yes

Yes  No

No