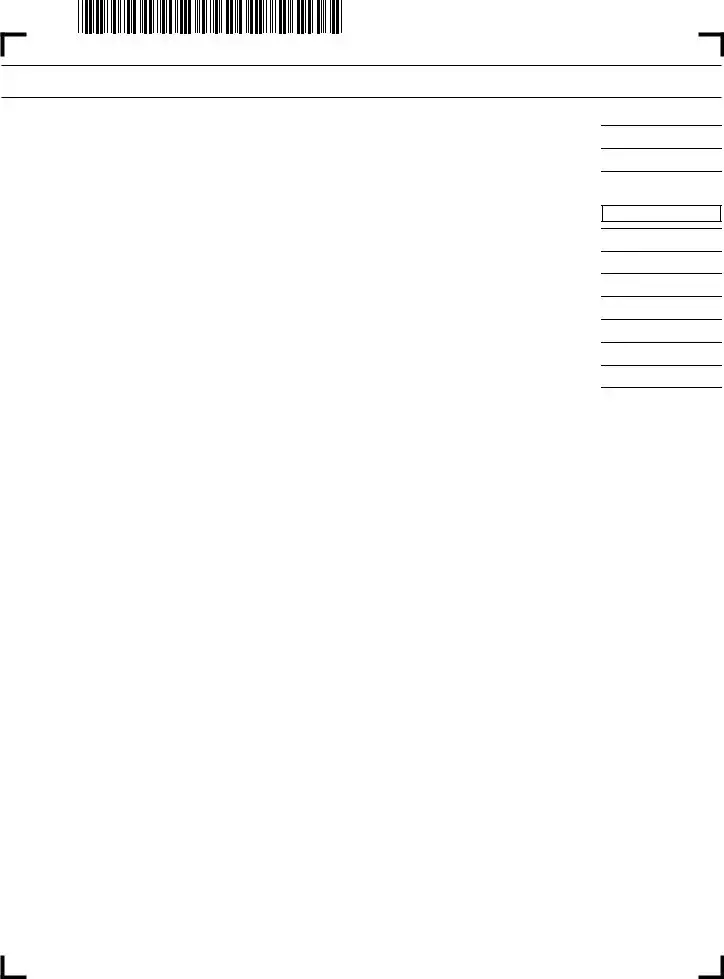

1 |

Enter taxable interest (other than interest from Massachusetts banks) received during the year |

1 |

2 |

Enter taxable dividends received during the year |

2 |

3 |

Add lines 1 and 2 |

3 |

4 |

Enter taxable interest (other than interest from Massachusetts banks) and dividends from all partnerships and |

|

|

non-Massachusetts estates and trusts |

4 |

5Subtotal. Add lines 3 and 4. If you have no short-term capital gains or losses, long-term gains on collectibles and pre-1996 installment sales, carryover short-term losses from prior years, or net long-term capital losses, omit lines 6 through 27.

Enter this amount in line 28 and on Form 3M, line 2. Omit lines 29 and 30. Otherwise complete Schedule B. . . . . . . . . . . 5

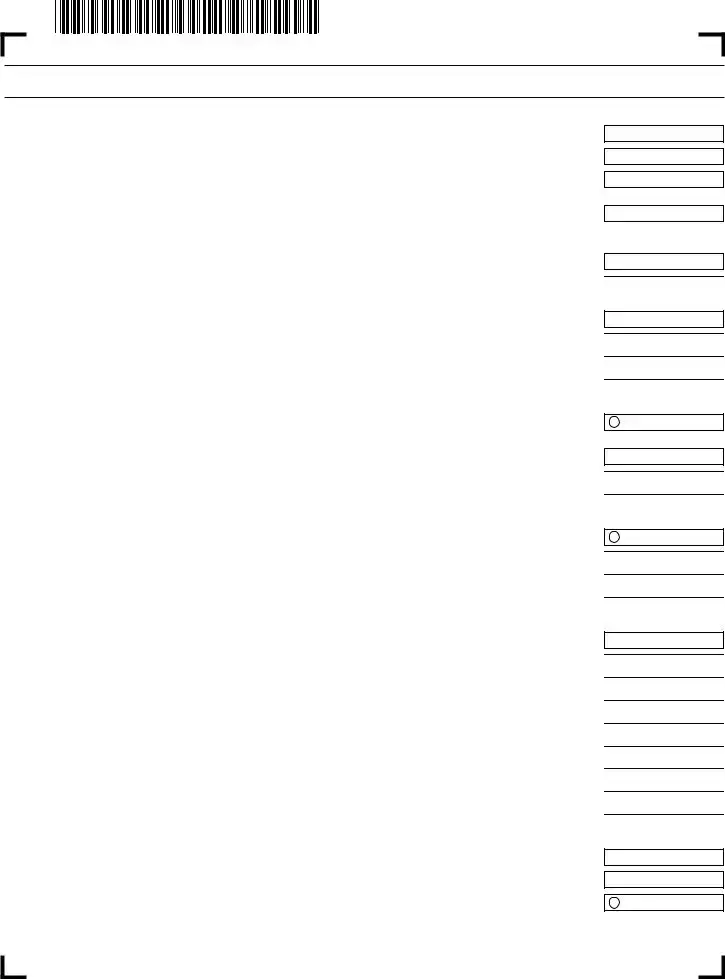

6 Short-term capital gains (included in U.S. Schedule D, lines 1 through 5, col. h) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7Long-term capital gains on collectibles and pre-1996 installment sales (from Massachusetts Schedule D, line 11;

see Form 1 instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

8 Add lines 6 and 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8  9 Short-term capital losses (included in U.S. Schedule D, lines 1 through 5, col. h) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

9 Short-term capital losses (included in U.S. Schedule D, lines 1 through 5, col. h) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9  10 Prior short-term losses for years beginning after 1981 (from 2020 Massachusetts Schedule B, line 30) . . . . . . . . . . . . . . 10

10 Prior short-term losses for years beginning after 1981 (from 2020 Massachusetts Schedule B, line 30) . . . . . . . . . . . . . . 10

11Combine lines 8 through 10. If 0 or greater, omit lines 12 through 15 and enter this amount in line 16.

If the total is a loss, go to line 12. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

12Short-term losses applied against interest and dividends. Enter the smaller of line 5 or line 11 (as a positive amount).

Not more than $2,000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

13 Subtotal. Combine lines 11 and 12 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Short-term capital losses applied against long-term capital gains (see instructions).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

14 Short-term capital losses applied against long-term capital gains (see instructions).. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

15Short-term losses available for carryover in 2022. Combine lines 13 and 14 and enter result here and in line 30,

omit lines 16 through 20 and complete lines 21 through 29 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Short-term gains and long-term gains on collectibles. Enter amount from line 11 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16  17 Long-term capital losses applied against short-term capital gains (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

17 Long-term capital losses applied against short-term capital gains (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17  18 Subtotal. Subtract line 17 from line 16. Enter result here. If line 18 is 0, omit line 19, and enter 0 in line 20. . . . . . . . . . . . 18

18 Subtotal. Subtract line 17 from line 16. Enter result here. If line 18 is 0, omit line 19, and enter 0 in line 20. . . . . . . . . . . . 18

19Long-term gains deduction. Complete only if lines 7 and 18 are greater than 0. If line 7 shows a gain, enter 50%

of line 7 minus 50% of losses in lines 9, 10 and 17, but not less than 0 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

20 Short-term gains after long-term gains deduction. Subtract line 19 from line 18. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20  21 Enter the amount from line 5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

21 Enter the amount from line 5. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21  22 Short-term losses applied against interest and dividends. Enter the amount from line 12 . . . . . . . . . . . . . . . . . . . . . . . . . 22

22 Short-term losses applied against interest and dividends. Enter the amount from line 12 . . . . . . . . . . . . . . . . . . . . . . . . . 22  23 Subtotal. Subtract line 22 from line 21 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

23 Subtotal. Subtract line 22 from line 21 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23  24 Long-term losses applied against interest and dividends (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

24 Long-term losses applied against interest and dividends (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24  25 Adjusted interest and dividends. Subtract line 24 from line 23 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

25 Adjusted interest and dividends. Subtract line 24 from line 23 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25  26 Enter the amount from line 20. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

26 Enter the amount from line 20. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26  27 Adjusted gross interest, dividends and certain capital gains and losses. Add lines 25 and 26. Not less than 0 . . . . . . . . . 27

27 Adjusted gross interest, dividends and certain capital gains and losses. Add lines 25 and 26. Not less than 0 . . . . . . . . . 27

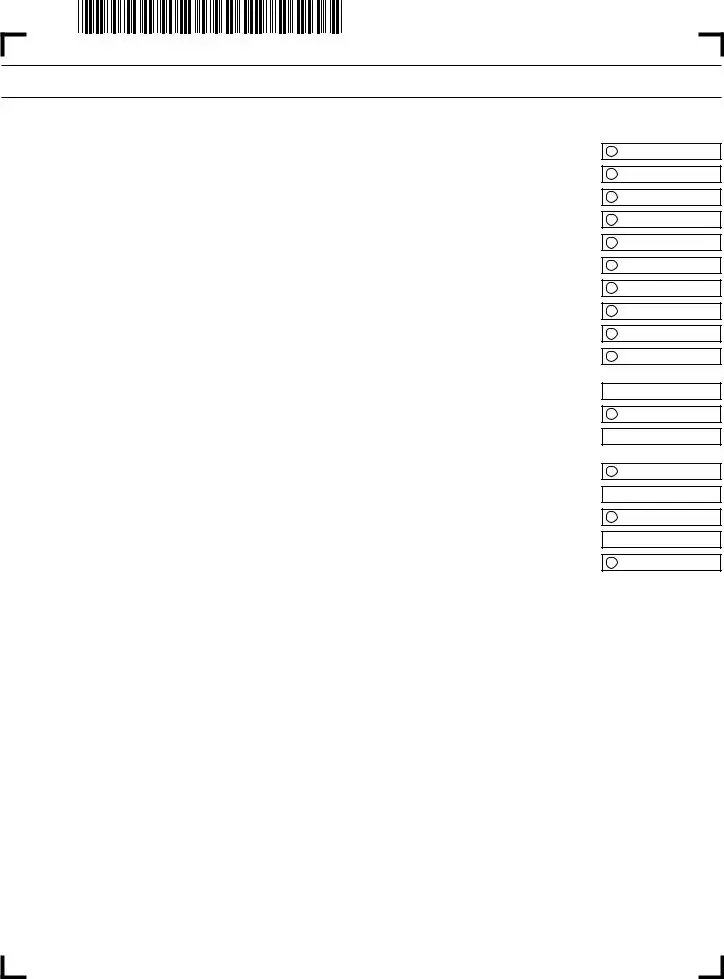

28If line 27 is greater than or equal to line 5, enter the amount from line 5 here and on Form 3M, line 2. If line 27 is

|

less than line 5, enter line 27 here and on Form 3M, line 2 |

28 |

29 |

Taxable 12% capital gains. Subtract line 28 from line 27. Not less than 0. Enter result here and on Form 3M, line 5 |

29 |

30 |

Available short-term losses for carryover in 2022. Enter amount from line 15 only if it is a loss |

30 |