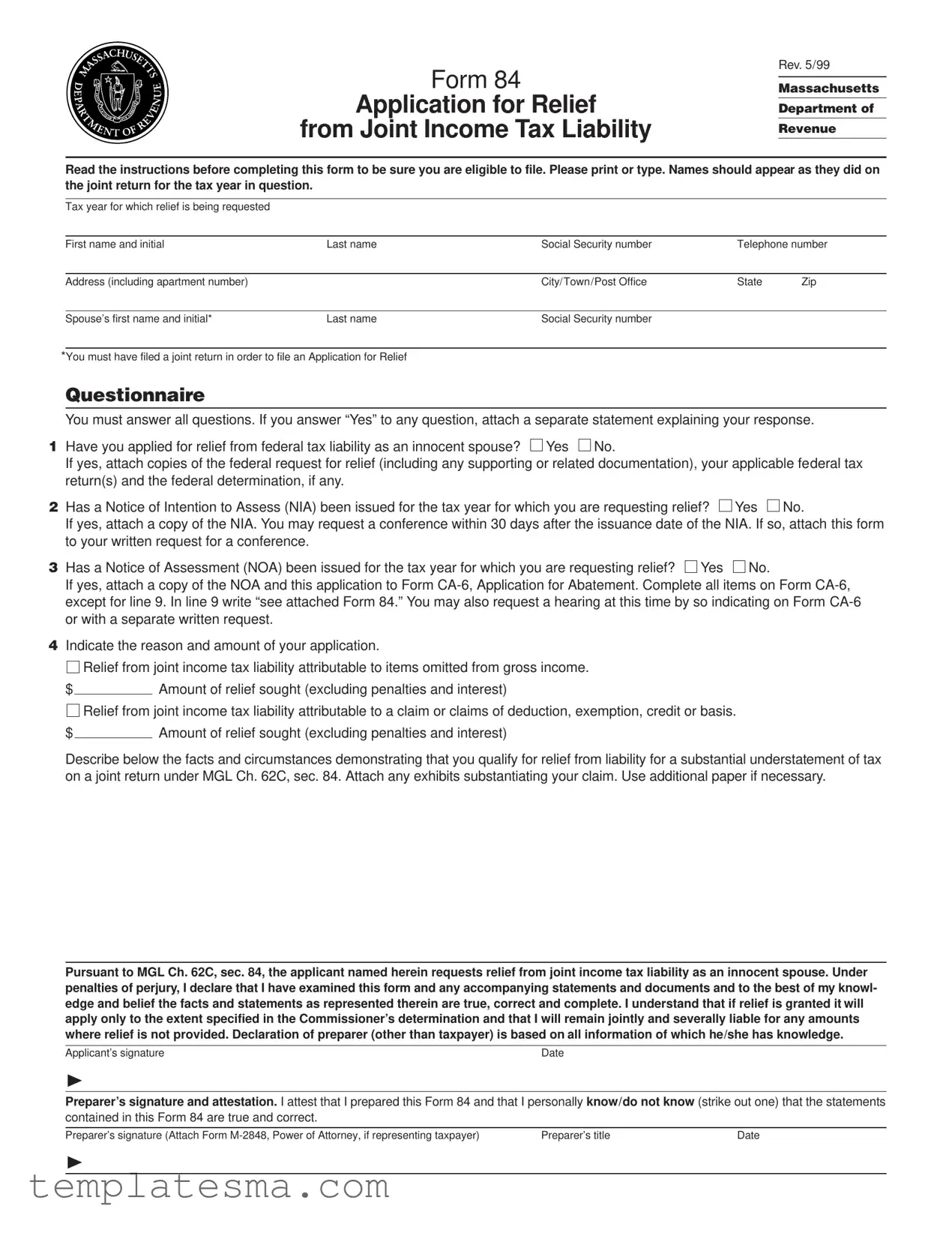

What is Form 84 and who needs to file it?

Form 84, also known as the Application for Relief from Joint Income Tax Liability, is a document used in Massachusetts for individuals seeking relief from taxes filed jointly with a spouse. It's specifically for those who believe they should not be held responsible for inaccuracies or understated tax amounts due to their spouse's actions. You need to file this form if you were unaware of the mistake on your joint tax return and it would be unfair to hold you liable.

When should Form 84 be submitted to the Massachusetts Department of Revenue?

Form 84 must be submitted either in response to a Notice of Intention to Assess (NIA) within 30 days of its issuance or after receiving a Notice of Assessment (NOA), by attaching it to a completed Form CA-6, Application for Abatement. The timing is crucial to ensure your application is considered.

What information is required when completing Form 84?

While filling out Form 84, you must provide names as they appeared on the joint return, tax year in question, your contact information, and detailed information on why you are seeking relief. Additionally, if you answer "Yes" to any questions in the questionnaire section, you must attach a detailed explanation along with any relevant supporting documents.

Can I file Form 84 without applying for federal relief as an innocent spouse?

Yes, you can file Form 84 without applying for federal relief as an innocent spouse; however, if you have applied for federal relief, you must attach copies of the federal request, any related documentation, and the federal determination to your Form 84 application.

What constitutes a "substantial understatement" for the purposes of Form 84?

A substantial understatement refers to an amount of understated tax, excluding interest and penalties, that exceeds $200 for omitted items from gross income, or exceeds $500 for claims of deductions, exemptions, credits, or basis without factual or legal basis. This criterion helps determine eligibility for relief.

How is "inequitable liability" determined for applicants of Form 84?

Inequitable liability is determined by examining all the facts and circumstances of the case. Factors like whether the applicant significantly benefited from the understatement play a crucial role in this determination. No single factor is decisive, but the overall fairness of holding the applicant liable is assessed.

What happens after Form 84 is approved?

Once Form 84 is approved, the Massachusetts Department of Revenue will issue a written determination specifying the extent of relief granted. The applicant will then be relieved from the specified joint tax liabilities, and any overpaid taxes will be refunded. However, the applicant remains liable for any part of the tax not covered by the relief, and the other spouse remains fully liable for the tax.

Is it possible to request a hearing or conference about my Form 84 application?

Yes, if you have received a Notice of Intention to Assess (NIA), you may request a conference within 30 days of its issuance by attaching Form 84 to your written request. If you received a Notice of Assessment (NOA), you can request a hearing by indicating so on Form CA-6 or through a separate written request when you submit your application. This is an opportunity to discuss your application and seek any clarifications.

Yes

Yes  No.

No. Yes

Yes  No.

No. Yes

Yes  No.

No.

Relief from joint income tax liability attributable to items omitted from gross income.

Relief from joint income tax liability attributable to items omitted from gross income.