Instructions

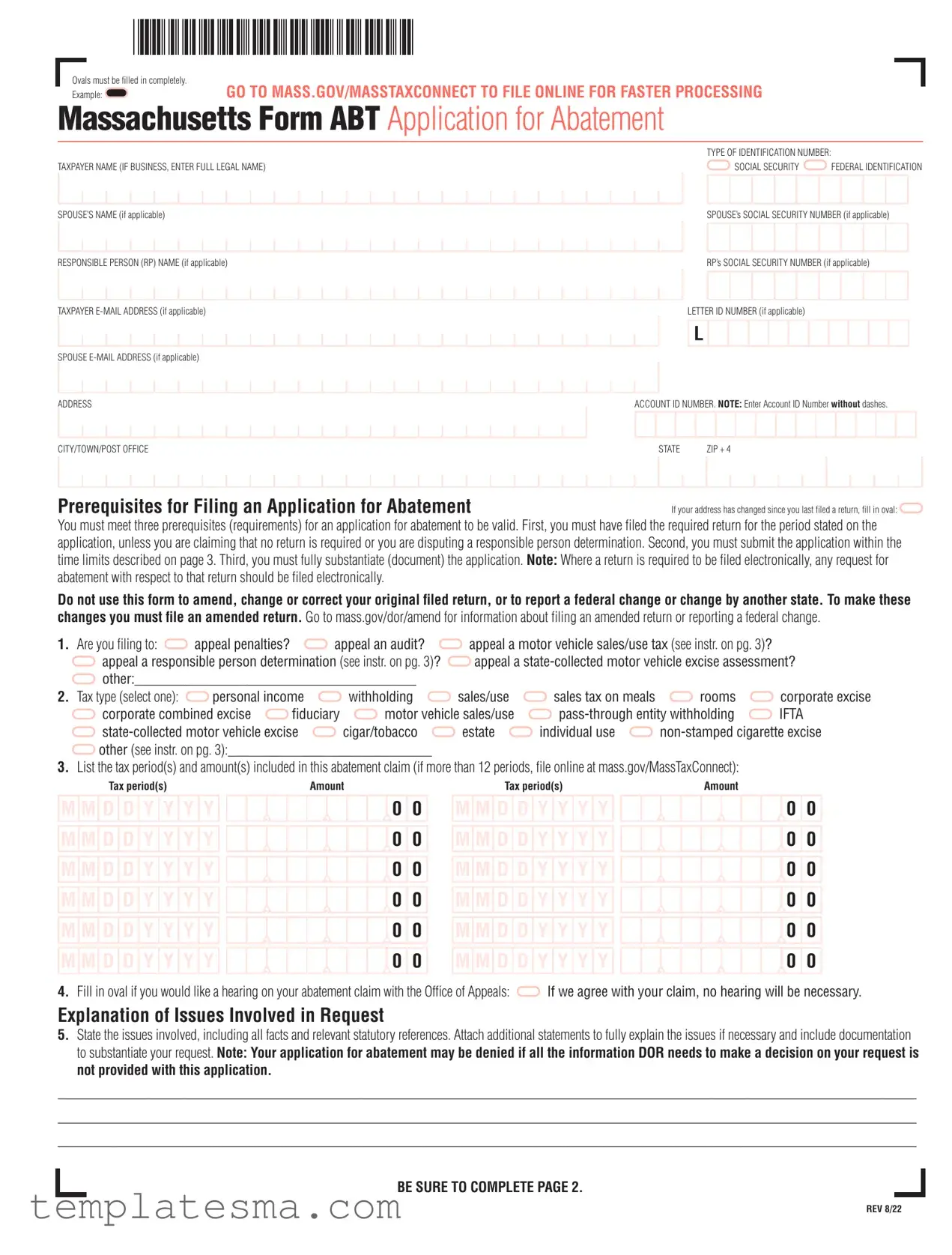

Taxpayer Information. Use a separate Form ABT for each location and account. The Letter ID number and Account ID number will help us understand your appeal. The Letter ID, beginning with L, can be found in the top right-hand corner of most DOR notices. The Account ID number might be found in the top right-hand corner of a notice or in the text of the notice. It can also be found on MassTaxConnect, and you can file there as well under “File an Appeal.” The Account ID number looks like XXX-12345678-999 where the

XXXrepresents three alphabet letters and the rest are digits. Note: Enter the Account ID number on Form ABT without dashes. An Account ID is required except for Motor Vehicle Sales Tax and Deeds Excise appeals.

If you are appealing a responsible person determination, see section below.

Line 1. Use this form to appeal an audit assessment; request waiver of penalties; request innocent spouse relief; challenge a responsible person determination; or request an abatement of motor vehicle excise or motor vehicle sales or use tax billed by DOR. Do not use this form to amend, change or correct your original filed return, or to report a federal change or change by another state. To make these changes you must file an amended return. Go to mass.gov/dor/amend for information about filing an amended return or reporting a federal change.

Line 2. Choose only one tax type. If appealing more than one tax type, file a separate Form ABT for each one. If your tax type is not listed, choose "Other," which includes but is not limited to alcoholic beverage excise, sales tax on telecommunication services, and pass-through entity excise.

Line 3. If you have more than 12 tax periods in this abatement claim, file online at mass.gov/MassTaxConnect.

Line 5. Explain why you are requesting an abatement and attach all information necessary to support your claim. Be sure to attach Form 84, Application for Relief From Joint Income Tax Liability, if requesting innocent spouse relief. You can find guidance about appropriate documentation in DOR’s online Tax Guides at mass.gov/dor or call us at (617) 887-MDOR or toll-free in Massachusetts 1-800-392-6089.

Time limits:

You must submit your application for abatement to DOR within the time limits provided in MGL ch 62C, § 37. Generally, this means:

a.Within three years from the date of the filing of the return (or within three years from the due date, if the return was filed before the due date).

b.Within two years from the date the tax was assessed or deemed to be assessed;

c.Within one year from the date the tax was paid;

d.Within two years of DOR’s determination of a responsible person’s liability;

e.Within any agreed-upon extension of time for assessment of taxes under MGL ch 62C, § 27.

Note: For an Application for Relief from Joint Income Tax Liability, review the time limits for filing under MGL ch 62C, § 84.

Additional information

To give DOR permission to discuss this application with someone other than you, complete the Power of Attorney section.

Interest and, in some cases, penalties will accrue on any unpaid amounts. Although collection activity will generally be suspended during the appeal process, you may wish to pay the amount you are appealing to stop the

accrual of interest and penalties. Note: In some cases DOR is allowed to abate penalties, but is not generally allowed to abate interest. If the abatement is approved after the assessment has been paid, a refund, with applicable interest, will be issued.

To request settlement consideration, submit Form DR-1, Office of Appeals Form, with this application for abatement. See AP 628 at mass.gov/dor/ appeals.

Important Information if Appealing Tax on a Motor Vehicle

Are you appealing the amount of sales tax paid when registering a motor vehicle?

The Registry of Motor Vehicles (RMV) and Department of Revenue (DOR) must follow Massachusetts law in determining the amount of sales tax to be paid. The amount must be the higher of the National Automobile Dealers Association (NADA) value of the vehicle as published in the Used Car Guide as “clean trade-in” value or actual price paid for the vehicle. The condition of the car has no additional impact on how the sales tax is determined.

When should I appeal the amount of motor vehicle sales or use tax?

If the sales tax charged was incorrectly calculated for the motor vehicle purchased or if the sales tax charged was on a motor vehicle that you believe should have been an exempt transfer or purchase. For example, if the NADA “clean trade-in” value used in the calculation was not specifically for the car you purchased. Or, if the actual price paid for the vehicle, as used in the calculation, was an incorrect amount. Those are good reasons to appeal the sales tax.

What if I think the NADA value is too high based on the condition of the car?

Massachusetts law requires the RMV to use the higher of the NADA value or the purchase price in determining the sales tax. The Department of Revenue cannot take the condition of the vehicle into account when considering an abatement request. If the NADA value is higher than the purchase price, the NADA value must be used, regardless of the vehicle’s condition. DOR will not allow a different value.

Rescission or cancellation of sale

If the abatement request is related to a rescission of sale, attach copies of:

•Bill of sale;

•Paperwork from the RMV reflecting sales tax paid, charges for the title, and registration fee;

•Registration; and

•Completed Form MV-AB2, Affidavit – Rescission of Sale of a Motor Vehicle.

Important information if appealing a responsible person determination

•Taxpayer Name – enter the responsible person’s name.

•Taxpayer ID – enter the responsible person’s Social Security number.

•Responsible Person (RP) Name and RP Social Security number – enter the responsible person’s name and Social Security number again.

•Account ID Number is the Account ID for the business tax liability for the responsible person determination.

•In Line 1, fill in the bubble for “appeal a responsible person determination.”

•In Line 2, fill in the bubble for the tax type of the business tax liability for the responsible person determination.