Fill Your Massachusetts M 941A Form

Fill Your Massachusetts M 941A Form

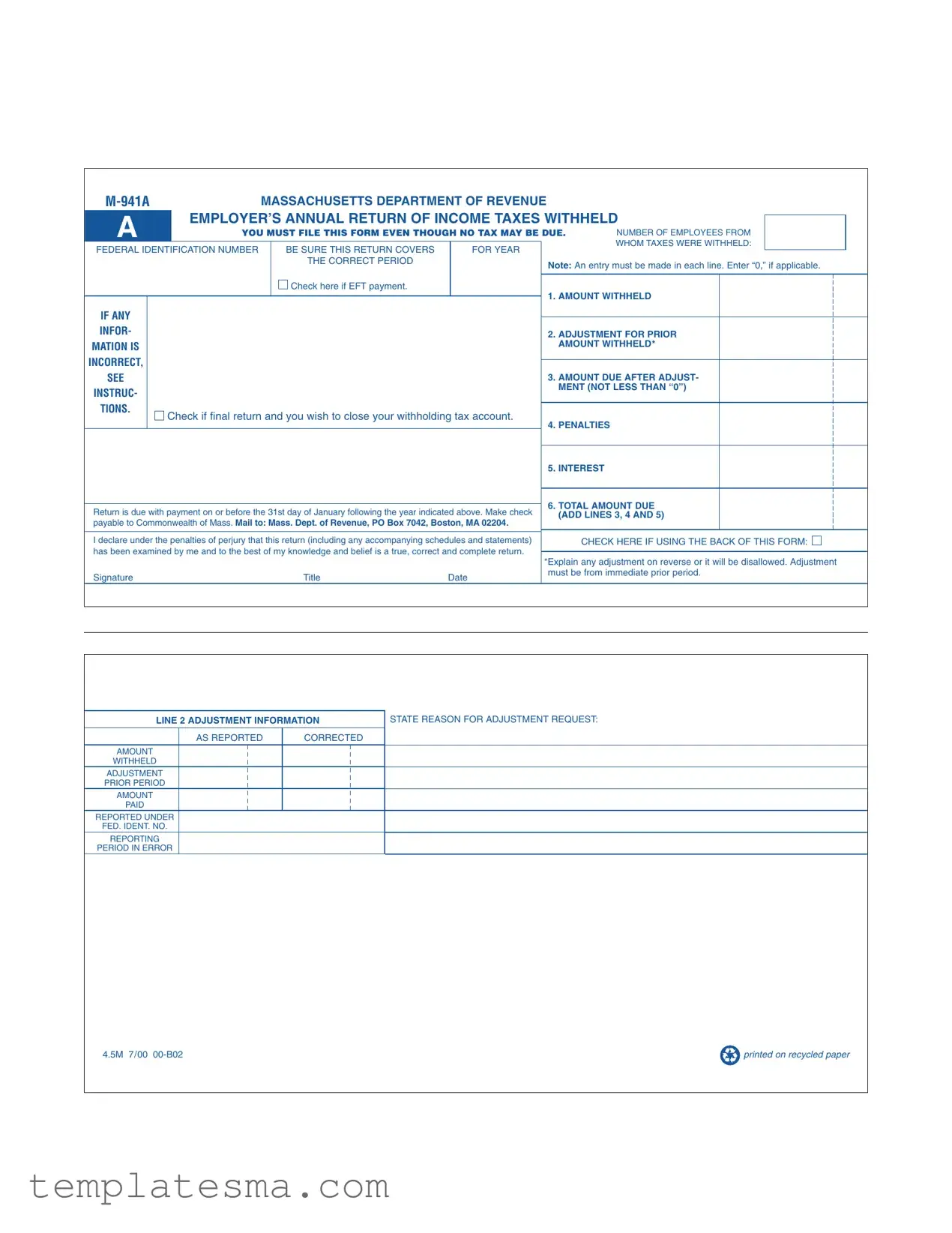

In the bustling world of business operations within Massachusetts, navigating through the intricate aspect of tax compliance is a crucial endeavor for every employer. The Massachusetts M 941A form emerges as a pivotal document designed by the Massachusetts Department of Revenue, serving as an annual return of income taxes withheld by employers. At the heart of this mandate is the requirement for every employer to file this form, regardless of whether taxes are due or not, highlighting its significance in the state’s tax administration. Its sections demand detailed information, including the number of employees from whom taxes were withheld, the total amount withheld, adjustments for prior amounts, and the final tally that dictates the amount due after considerations for any adjustments, penalties, or interest. Notably, the form demands accuracy and completeness, under the threat of penalties for perjury, if found otherwise. Timeliness is also key, with a specific due date set on or before the 31st day of January following the reporting year, underscoring the importance of punctuality in compliance. Furthermore, it allows for adjustments related to prior periods, a feature that acknowledges the dynamic nature of business and the complexities of payroll management. This form not only facilitates a straightforward annual reconciliation of income taxes withheld but also marks the end of a year's tax responsibilities for employers, with options to amend or close the withholding tax account if it is to be the final return. As businesses navigate through the fiscal year, understanding and correctly filing the Massachusetts M 941A form is an indispensable step in fulfilling state tax obligations.

|

MASSACHUSETTS DEPARTMENT OF REVENUE |

|

|

|

|

|||||||||

A |

|

EMPLOYER’S ANNUAL RETURN OF INCOME TAXES WITHHELD |

|

|

||||||||||

|

|

|

||||||||||||

|

YOU MUST FILE THIS FORM EVEN THOUGH NO TAX MAY BE DUE. |

NUMBER OF EMPLOYEES FROM |

|

|

||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

WHOM TAXES WERE WITHHELD: |

|

|

||

FEDERAL IDENTIFICATION NUMBER |

|

BE SURE THIS RETURN COVERS |

|

FOR YEAR |

|

|||||||||

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

THE CORRECT PERIOD |

|

|

|

Note: An entry must be made in each line. Enter “0,” if applicable. |

|||||

|

|

|

|

|

|

|

|

|

||||||

|

IF INCORRECT, SEE INSTRUCTIONSCheck. DOhereNOTif EFTALTERpayment. . |

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

1. AMOUNT WITHHELD |

|

|

|

||

BUSINESS |

NAME |

|

|

|

|

|

|

|

|

|

|

|

||

IF ANY |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

INFOR- |

|

|

|

|

|

|

|

2. ADJUSTMENT FOR PRIOR |

|

|

|

|||

BUSINESS |

ADDRESS |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

AMOUNT WITHHELD* |

|

|

|

|||||

MATION IS |

|

|

|

|

|

|

|

|

|

|

||||

INCORRECT, |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||

CITY/SEETOWN |

|

|

|

STATE |

ZIP |

|

|

3. AMOUNT DUE AFTER ADJUST- |

|

|

|

|||

INSTRUC- |

|

|

|

|

|

|

|

|

MENT (NOT LESS THAN “0”) |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||

TIONS. |

Check if final return and you wish to close your withholding tax account. |

|

|

|

|

|

||||||||

|

|

|

|

|

||||||||||

|

4. PENALTIES |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. INTEREST |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

6. TOTAL AMOUNT DUE |

|

|

|

||

Return is due with payment on or before the 31st day of January following the year indicated above. Make check |

||||||||||||||

(ADD LINES 3, 4 AND 5) |

|

|

|

|||||||||||

payable to Commonwealth of Mass. Mail to: Mass. Dept. of Revenue, PO Box 7042, Boston, MA 02204. |

|

|

|

|||||||||||

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|||||||||

I declare under the penalties of perjury that this return (including any accompanying schedules and statements) |

|

CHECK HERE IF USING THE BACK OF THIS FORM: |

||||||||||||

has been examined by me and to the best of my knowledge and belief is a true, correct and complete return. |

|

|

|

|

|

|||||||||

*Explain any adjustment on reverse or it will be disallowed. Adjustment |

||||||||||||||

|

|

|

|

|

|

|

|

|

||||||

Signature |

|

|

Title |

|

Date |

must be from immediate prior period. |

||||||||

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

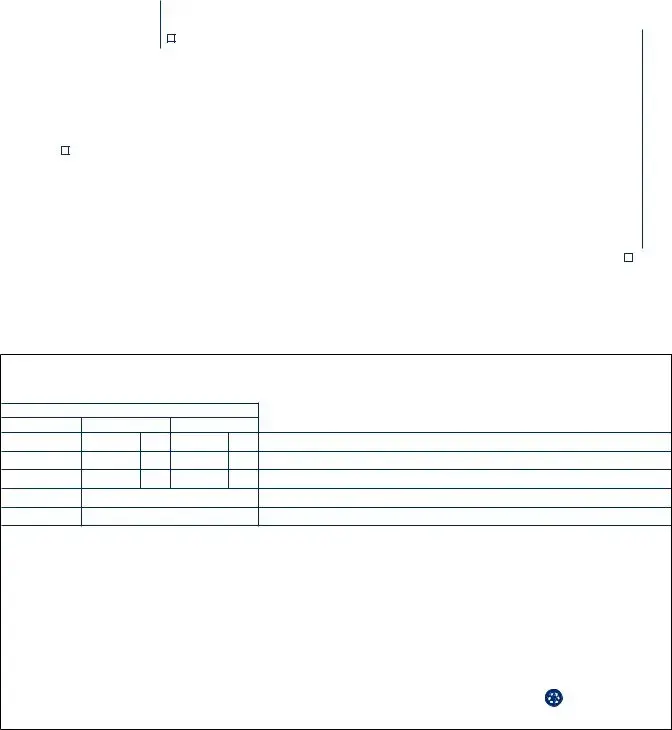

LINE 2 ADJUSTMENT INFORMATION |

STATE REASON FOR ADJUSTMENT REQUEST: |

|

AS REPORTED |

CORRECTED |

|

AMOUNT |

|

|

WITHHELD |

|

|

ADJUSTMENT |

|

|

PRIOR PERIOD |

|

|

AMOUNT |

|

|

PAID |

|

|

REPORTED UNDER |

|

|

FED. IDENT. NO. |

|

|

REPORTING |

|

|

PERIOD IN ERROR |

|

|

4.5M 7/00 |

|

printed on recycled paper |

| Fact | Description |

|---|---|

| Form Name | M-941A |

| Issuing Body | Massachusetts Department of Revenue |

| Title | Employer’s Annual Return of Income Taxes Withheld |

| Filing Requirement | Required to be filed even if no tax is due. |

| Key Information Needed | Number of employees, Federal Identification Number, Amount Withheld, and Adjustments for Prior Amount Withheld. |

| Governing Law | Massachusetts State Tax Law |

| Due Date | On or before the 31st day of January following the year indicated on the form. |

Filing the Massachusetts M-941A form is an essential duty for employers in Massachusetts, summarizing the income taxes they've withheld from employees over the past year. It serves as an annual reconciliatory document to ensure the correct amount of tax has been collected and forwarded to the state. This form is crucial for maintaining compliance with state tax laws, and filling it out accurately is paramount. Below are clear, step-by-step instructions to guide you through the completion of this form.

After filling out the form according to these steps, you have completed your duty in accurately reporting and reconciling the income taxes withheld from your employees. Ensuring the form is filled out carefully and submitted on time is vital for compliance with Massachusetts state tax laws, helping avoid potential fines or penalties.

What is the Massachusetts M 941A form?

The Massachusetts M 941A form is a document that employers in Massachusetts must fill out and submit to the state's Department of Revenue. It's an annual return form for income taxes that have been withheld from employees' wages. Employers are required to file this form each year, even if no tax is due.

Who needs to file the M 941A form?

Any employer that has withheld income taxes from employees' wages in Massachusetts is required to file the M 941A form. This includes businesses of all sizes, whether they have withheld taxes for one employee or for many employees.

When is the M 941A form due?

The M 941A form must be submitted to the Massachusetts Department of Revenue on or before January 31st following the year in which the income taxes were withheld.

What should I do if I find a mistake in the information provided on the M 941A form?

If you discover that any information on the M 941A form is incorrect, you should look at the instructions provided with the form for guidance on how to make corrections. Generally, adjustments can be made for prior amounts withheld by entering the corrected information in the designated area on the form. There's a section for explaining adjustments, and it's important to provide a clear reason for any changes.

How do I make a payment along with the M 941A form?

Payments can be made by check accompanying the form submission. Checks should be made payable to the Commonwealth of Massachusetts and mailed to the address listed on the form. If using electronic funds transfer (EFT), there's an option to indicate this choice on the form as well.

What do I do if I need to close my business's withholding tax account?

There's a checkbox on the M 941A form specifically for employers who wish to close their withholding tax account in conjunction with filing their annual return. You should check this box if you're submitting your final return and want the Department of Revenue to close your account.

What if no taxes were withheld during the year?

Even if no taxes were withheld during the year, employers are still required to file the M 941A form. In this case, you should enter “0” in the relevant lines to indicate that no taxes were withheld.

Where do I mail the completed M 941A form?

The completed M 941A form, along with any payment due, should be mailed to the Massachusetts Department of Revenue at PO Box 7042, Boston, MA 02204. It's important to ensure that the form is mailed by the due date to avoid any penalties or interest.

Filling out the Massachusetts M 941A form, an employer’s annual return of income taxes withheld, necessitates careful attention to detail to ensure accuracy. Unfortunately, errors can occur, which may lead to complications or delays with the Massachusetts Department of Revenue. Below are five common mistakes made during this process:

Not filing the form when no tax is due: Employers sometimes assume that if no taxes were withheld during the year, they do not need to file the M 941A form. This assumption is incorrect as the form must be filed regardless of whether any tax is due.

Incorrect information about the business: Often, errors are made in the section detailing the business name, address, city/town, state, and ZIP. Ensuring this information is accurate and current is crucial as it can affect the receipt of necessary correspondence from the Department of Revenue.

Failing to report the exact number of employees: The form requires employers to state the number of employees from whom taxes were withheld. An inaccurate count can lead to discrepancies and potential audits.

Miscalculating the amounts: Mistakes in the calculation of the amount withheld, adjustments from the previous period, and the total amount due (including penalties and interest, if any) are common. These mistakes can either be due to simple mathematical errors or a misunderstanding of how adjustments are applied.

Omitting signature and date: A frequent overlook by filers is failing to sign and date the form. The signature and the date confirm the filer's declaration that the information provided is complete and accurate to the best of their knowledge, under the penalties of perjury. An unsigned form is considered incomplete and can lead to processing delays.

To navigate these pitfalls, it is advisable to double-check all entries on the form, consult the instructions provided by the Massachusetts Department of Revenue for clarity, and consider professional assistance if there are uncertainties. Removing these common errors can streamline the process, ensuring compliance and minimizing any potential disruptions in the business’s operations.

When dealing with the Massachusetts M-941A form, an employer's annual return of income taxes withheld, there are several other forms and documents that often accompany it to ensure compliance and accurate tax reporting. Understanding these additional forms can help businesses manage their tax obligations efficiently.

Each of these documents plays a specific role in the overall tax reporting and withholding process, ensuring both the state and federal tax obligations are met. By maintaining accurate and timely filings of these forms, employers can avoid penalties and ensure their businesses run smoothly.

The Massachusetts M 941A form is similar to the Federal Form 941, which is known as the Employer's Quarterly Federal Tax Return. Both forms are pivotal for employers as they report the income taxes, social security tax, and Medicare tax withheld from employees' wages. Additionally, they both require employers to calculate and report their portion of Social to security and Medicare taxes. The main difference lies in the frequency of reporting. The M 941A is an annual form, specifically for Massachusetts' employers to report state income tax withheld, whereas the Federal Form 941 is filed quarterly. This distinction is important for business owners to recognize to ensure compliance with both state and federal tax obligations.

Another document that bears resemblance to the M 941A is the Form W-3, the Transmittal of Wage and Tax Statements. This form, used on a federal level, summarizes the information included on the Form W-2s, which report wages, tips, and other compensation paid to employees and the taxes withheld from them. Like the M 941A, the Form W-3 is an annual summary report. However, Form W-3 deals with the transmission of personal employee tax information to the Social Security Administration alongside copies of Form W-2, rather than being a report to the Department of Revenue. Both forms serve as a comprehensive year-end closure on withheld taxes, yet they cater to different governmental entities and purposes.

Additionally, the M 941A parallels the state's own Quarterly Wage Report forms that employers must submit during the year. These documents, often referred to by their state-specific form numbers, such as Form M-941 in Massachusetts, require similar information on wages paid and taxes withheld for each employee. The principal difference is the period the forms cover. While the Quarterly Wage Reports necessitate filing four times a year, offering a segmented view of an employer's tax obligations, the annual M 941A provides a cumulative perspective. This similarity in content but difference in reporting timeframe helps businesses track their payroll expenses and tax liabilities throughout the year before summarizing annually on the M 941A.

When preparing the Massachusetts M-941A form, employers should adhere to a set of recommended practices to ensure accuracy and compliance with state tax laws. Attention to detail can prevent common mistakes and facilitate a smoother process. Below are outlined dos and don'ts that are crucial for correctly filling out the form.

Do:

Don't:

There are several common misconceptions about the Massachusetts M 941A form, which is essential for employers when filing their annual return of income taxes withheld. Understanding these misconceptions can ensure compliance with state tax obligations and avoid potential penalties. Here are five key misconceptions:

Understanding these common misconceptions about the Massachusetts M 941A form helps employers accurately meet their tax reporting obligations, reducing the risk of errors and ensuring compliance with state tax laws.

Understanding the Massachusetts M-941A form, which is the Employer’s Annual Return of Income Taxes Withheld, is crucial for employers in the state. Here are nine key takeaways to help guide you through the process of filling out and using this form.

Properly filling out and submitting the Massachusetts M-941A form is not only a matter of legal compliance but also a part of maintaining organized and accurate payroll and tax records. The above key points offer a foundational understanding to ensure compliance and accuracy in this annual fiscal responsibility.

Mpc 560 - Communication with the Division of Medical Assistance, particularly regarding estate recovery, underscores the petitioner's compliance with state obligations, a necessary step detailed in the MPC 160 form.

Massachusetts Aca 1202 - Physicians must attest to practicing in family medicine, general internal medicine, or pediatric medicine, including recognized subspecialties, to be eligible.