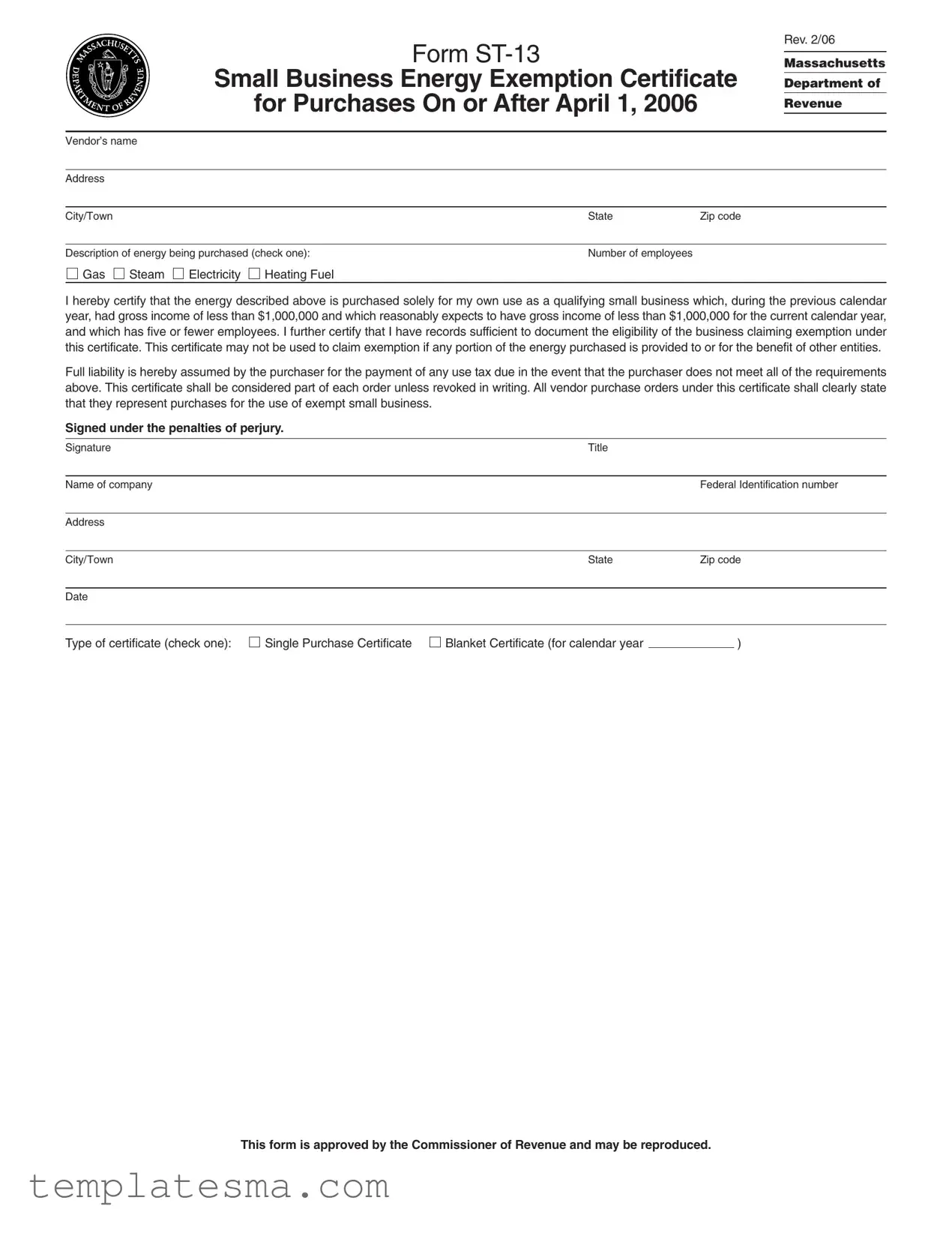

What is the Massachusetts ST-13 form?

The Massachusetts ST-13 form, also known as the Small Business Energy Exemption Certificate, is a document that allows qualifying small businesses to claim an exemption from paying sales tax on purchases of gas, steam, electricity, and heating fuel intended solely for their use. To qualify, a business must have had gross income of less than $1,000,000 in the previous calendar year and expects to have less than $1,000,000 in gross income in the current year, with five or fewer employees.

Who needs to fill out the Massachusetts ST-13 form?

Small business owners in Massachusetts who meet the specified criteria of having gross income less than $1,000,000 for the previous calendar year and the current calendar year, and who employ five or fewer employees, must fill out the Massachusetts ST-13 form. This includes businesses that are newly formed and reasonably expect to meet the income criteria for the current year.

How does a business qualify for the energy exemption?

To qualify for the energy exemption, a business must, during the previous calendar year, have gross income of less than $1,000,000 and reasonably expects to have gross income of less than $1,000,000 for the current calendar year. Additionally, the business must have five or fewer employees. The exemption is based on both income and the number of employees, and it must be claimed by submitting the ST-13 form to the vendor from whom the energy is purchased.

What are the responsibilities of vendors in regards to the ST-13 form?

Vendors are required to act in good faith when accepting the ST-13 form from purchasers claiming the small business energy exemption. They must retain a record of the sale, including the purchaser's name, address, and federal identification number, along with the sales price and a copy of the ST-13 form. This documentation is necessary to prove that the business is entitled to the small business exemption should it be required.

What should a business do if they no longer qualify for the exemption during the year?

If a business that has claimed a small business exemption under the ST-13 form ceases to qualify for this exemption due to changes in their income or number of employees, they are required to notify their vendor in writing. Failure to notify the vendor could result in the liability of use tax payment for the business on ineligible purchases.

Are there penalties for misuse of the ST-13 form?

Yes, willful misuse of the ST-13 form may result in criminal tax evasion penalties. These penalties can include up to one year in prison and fines up to $10,000 for individuals and $50,000 for corporations. It is important for businesses to ensure they fully meet the criteria and maintain accurate records when claiming this exemption to avoid any potential penalties.