Printable Massachusetts Promissory Note Form

Printable Massachusetts Promissory Note Form

In Massachusetts, the Promissory Note form is a pivotal document for both lenders and borrowers involved in a financial transaction. This legal instrument outlines the terms and conditions under which money is lent and the commitment made by the borrower to repay the debt according to these specified terms. Not only does it detail the loan amount and repayment schedule, but it also addresses interest rates, late fees, and the consequences of failing to meet the agreed-upon payments. Essential for ensuring clarity and protection for all parties involved, the form serves as a formal acknowledgment of the debt and plays a critical role in personal and business finances. Its use spans a wide range of scenarios, from simple loans between family members to more complex financing arrangements between businesses. Understanding its major aspects is fundamental for anyone looking to navigate the intricacies of borrowing or lending money in Massachusetts, ensuring that all legal requirements are met and the interests of both parties are safeguardly addressed.

Massachusetts Promissory Note Template

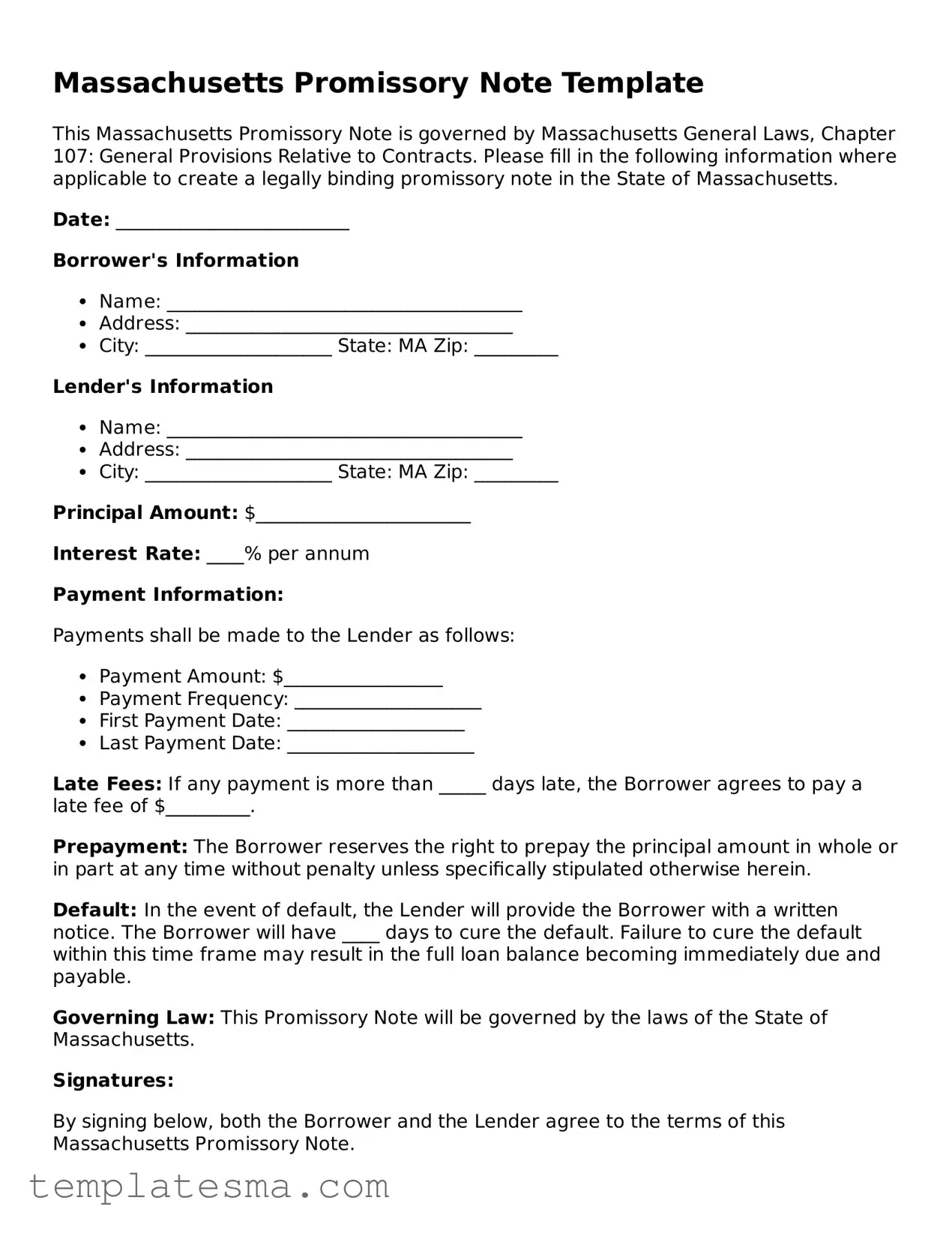

This Massachusetts Promissory Note is governed by Massachusetts General Laws, Chapter 107: General Provisions Relative to Contracts. Please fill in the following information where applicable to create a legally binding promissory note in the State of Massachusetts.

Date: _________________________

Borrower's Information

Lender's Information

Principal Amount: $_______________________

Interest Rate: ____% per annum

Payment Information:

Payments shall be made to the Lender as follows:

Late Fees: If any payment is more than _____ days late, the Borrower agrees to pay a late fee of $_________.

Prepayment: The Borrower reserves the right to prepay the principal amount in whole or in part at any time without penalty unless specifically stipulated otherwise herein.

Default: In the event of default, the Lender will provide the Borrower with a written notice. The Borrower will have ____ days to cure the default. Failure to cure the default within this time frame may result in the full loan balance becoming immediately due and payable.

Governing Law: This Promissory Note will be governed by the laws of the State of Massachusetts.

Signatures:

By signing below, both the Borrower and the Lender agree to the terms of this Massachusetts Promissory Note.

Borrower's Signature: _____________________________ Date: ____/____/______

Lender's Signature: _______________________________ Date: ____/____/______

| Fact | Details |

|---|---|

| 1. Purpose | The Massachusetts Promissory Note form is used for agreeing to pay back a loan within a specific time frame. |

| 2. Types | There are two main types: secured and unsecured. Secured means collateral backs the loan; unsecured does not. |

| 3. Interest Rates | The interest rate must be agreed upon by all parties and cannot exceed the state's maximum legal rate. |

| 4. Governing Law | The form and agreement are regulated by Massachusetts state law. |

| 5. Signatories | Both the borrower and the lender must sign the form, acknowledging their understanding and agreement. |

| 6. Co-signer | Adding a co-signer is an option for additional security, especially for unsecured loans. |

| 7. Default Consequences | If the borrower defaults, the consequences can range from late fees to legal action, depending on the terms set forth in the form. |

When you're about to fill out a Massachusetts Promissory Note form, it's like you're preparing a promise in writing. This document is typically used when money is being loaned, ensuring that the borrower agrees to pay back the lender under specific terms. There's no need to feel overwhelmed by the process. By following a series of straightforward steps, you can complete the form accurately and efficiently, making sure both parties are protected and clear about the agreement's expectations.

Once the form is completed and signed, both parties should keep a copy for their records. This will serve as a legal document that proves the existence of the loan and the terms agreed upon. Should any questions or issues arise regarding the loan, the promissory note will be an essential reference to resolve them. Remember, filling out this form accurately is a step toward ensuring a smooth financial transaction and maintaining a positive relationship between the lender and borrower.

What is a Massachusetts Promissory Note and why is it important?

A Massachusetts Promissory Note is a legal document that outlines a promise by one party to pay another party a certain sum of money, either at a future date or on demand. It's important because it clearly sets the terms of the loan, such as the amount borrowed, interest rate, and repayment schedule, which helps to prevent misunderstandings and legally enforces the agreement between the lender and the borrower.

Do I need a lawyer to create a Promissory Note in Massachusetts?

While it is not a requirement to have a lawyer to create a Promissory Note in Massachusetts, consulting with one can ensure that the document meets all legal requirements and protects the interests of both parties. A lawyer can also advise on specific terms to include that might be unique to your situation.

Can I write my own Promissory Note in Massachusetts, and is it legally binding?

Yes, you can write your own Promissory Note in Massachusetts, and as long as it contains all the necessary elements, it is considered legally binding. These elements include the amount of money borrowed, interest rate, repayment schedule, and the signatures of both parties. However, it's advisable to follow a template or seek legal advice to ensure all necessary information is correctly included.

What are the necessary elements to include in a Massachusetts Promissory Note?

A valid Massachusetts Promissory Note should include the date of the note, amount of money borrowed, interest rate, repayment terms (including dates and amounts), information about both the borrower and the lender, and signatures of both parties. Including these elements ensures the note’s enforceability in court, should disputes arise.

How is interest calculated on a Promissory Note in Massachusetts?

The interest on a Promissory Note in Massachusetts is typically calculated based on an annual percentage rate. The specific rate can be agreed upon by both parties but must not exceed the state’s maximum legal rate. It's crucial to clearly state how the interest is calculated in the note to avoid any confusion.

What happens if a Promissory Note is violated in Massachusetts?

If the borrower fails to follow the agreed repayment schedule, the lender has the right to take legal action to collect the debt. This might include filing a lawsuit to recover the money owed. The specific recourse available to the lender will depend on the terms of the Promissory Note and Massachusetts law.

Can a Massachusetts Promissory Note be modified after it's signed?

Yes, a Massachusetts Promissory Note can be modified, but any changes must be agreed upon by both the lender and the borrower. It's best to make any amendments in writing and have both parties sign the revised document to ensure the changes are legally binding.

Is a Promissory Note secured or unsecured, and what's the difference?

A Promissory Note in Massachusetts can be either secured or unsecured. A secured note is backed by collateral, meaning the borrower pledges an asset like a house or car that the lender can seize if the loan is not repaid. An unsecured note is not backed by collateral and is based solely on the borrower’s promise to pay. The main difference lies in the level of risk for the lender; secured notes offer a way to recover the loaned amount if the borrower defaults, while unsecured notes do not.

Filling out the Massachusetts Promissory Note form necessitates attention to detail and an understanding of what is required. Unfortunately, mistakes can happen, particularly when one is unfamiliar with the process. Listed below are five common errors individuals often make during this procedure. Recognizing these pitfalls can help ensure the process goes smoothly and that the document is legally binding and accurate.

Not Specifying the Terms Clearly: One of the most critical aspects of the Promissory Note is the clarity of the loan terms. This includes the loan amount, interest rate, repayment schedule, and due date. Failing to delineate these terms explicitly can lead to misunderstandings or legal disputes down the line.

Omitting the Interest Rate: In Massachusetts, if the Promissory Note does not specify an interest rate, the loan may still be subject to the state's statutory interest rate. However, neglecting to include this information can create confusion regarding the total amount owed over time.

Forgetting to Include Signatures: The Promissory Note must be signed by both the borrower and the lender to be legally binding. Sometimes, individuals complete the form but overlook this vital step, rendering the document unenforceable.

Ignoring Legal Requirements: Each state has its own legal requirements for Promissory Notes, and Massachusetts is no exception. Neglecting to adhere to these can result in a document that doesn’t comply with state law, potentially making it invalid.

Not Keeping a Copy: After the Promissory Note is signed, both parties should keep a copy for their records. Failure to do so can lead to issues later on if there's a dispute or if one party needs to reference the agreement for any reason.

Avoiding these mistakes not only helps in completing the Massachusetts Promissory Note form correctly but also ensures that the agreement between the borrower and lender is solid, transparent, and legally binding. Attention to detail and a thorough understanding of the requirements can prevent potential issues and foster a mutually beneficial relationship between the parties involved.

When handling financial transactions in Massachusetts, particularly those involving loans, a Promissory Note is a fundamental document. However, to ensure a comprehensive and protective approach, multiple supplemental documents are often utilized alongside the Promissory Note. These documents support, clarify, and provide legal safeguards for both the lender and the borrower. The following list includes some of the most common forms and documents used in conjunction with the Massachusetts Promissory Note.

These documents, when used collectively with a Promissory Note, create a robust legal framework that mitigates risks and establishes clear expectations for all parties involved in a financial transaction. For individuals navigating loans in Massachusetts, understanding and utilizing these documents effectively can ensure a secure and equitable lending process.

The Massachusetts Promissory Note form is similar to other legal documents used in financial transactions and lending agreements. These documents each have unique features, but share common purposes such as defining the terms of a loan, the obligations of each party, and the consequences of not meeting those obligations. Here, we'll delve into a couple of these documents and explore how they compare to a promissory note.

One document that bears resemblance to the Massachusetts Promissory Note is a Loan Agreement. Both serve as binding agreements between a lender and a borrower, outlining the loan's terms, repayment schedule, and interest rate. However, a Loan Agreement is often more comprehensive, including detailed clauses about the rights and duties of both parties, security interests, and what happens in case of default. The primary focus of a promissory note, in contrast, is to establish the borrower's promise to pay a specific sum of money to the lender under agreed conditions. While a promissory note can stand alone as a legal commitment to pay, a Loan Agreement provides a broader legal framework for the loan.

Another document similar to the promissory note is a Deed of Trust. In many ways, a Deed of Trust functions like a promissory note, particularly in its role in securing a loan for real property. The key difference lies in their mechanisms for handling defaults. A Deed of Trust involves three parties: the borrower, the lender, and a trustee, who holds the property's title as security for the loan. Should the borrower fail to uphold their repayment obligations, the trustee has the authority to sell the property to satisfy the debt. Promissory notes, while also detailing the repayment obligation, do not inherently involve a third-party trustee or direct stipulations for handling the property in the event of a default, unless specifically tied to a secured loan agreement or Deed of Trust.

When completing the Massachusetts Promissory Note form, being thorough and accurate is important. This document serves as a legal agreement between the borrower and the lender, detailing the loan's terms and the repayment plan. To ensure compliance and protect both parties' interests, follow these guidelines:

Do:Clearly identify both the lender and the borrower, including full names and addresses. This helps to avoid any confusion about the parties involved.

Specify the loan amount and interest rate explicitly to avoid any ambiguity. Include how the interest is calculated and any conditions that might affect the rate.

Outline the repayment schedule in detail. This should include due dates, the number of payments, and whether there is a grace period for late payments.

Sign and date the promissory note in the presence of a witness or notary. This formalizes the agreement and can provide additional legal validation.

Omit details about the loan's purpose. Although not always mandatory, including this information can clarify the loan's intent and ensure its proper use.

Forget to specify any collateral if the promissory note is secured. Detailing the collateral can expedite resolutions if the borrower defaults on the loan.

Ignore state laws regarding interest rates and lending practices. Adhering to these laws is crucial to ensure that the note is enforceable and complies with state regulations.

Leave blank spaces. To avoid alterations or disputes, fill in all sections of the form comprehensively and accurately.

When discussing the Massachusetts Promissory Note form, several misconceptions often arise. Understanding these can help in navigating financial agreements with more clarity and confidence.

One common misconception is that a promissory note and a loan agreement are the same. While they both relate to borrowing, a promissory note is more simplistic, outlining the amount owed and the repayment terms, whereas a loan agreement includes more detailed provisions.

Many believe that a notary's signature is always required for the form to be valid. While notarization can add a layer of authenticity, a promissory note in Massachusetts can be legally binding without it, as long as both parties sign the document.

Some think that only the borrower needs to sign the promissory note. However, for clarity and legal enforceability, it's prudent for both the lender and the borrower to sign.

There's also a misconception that promissory notes are for personal loans only. In reality, they can be used for a wide range of lending situations, including business loans.

Another incorrect assumption is that verbal agreements are just as binding as a written promissory note. While verbal contracts can be enforceable, a written note provides tangible evidence of the agreement’s terms and conditions.

Some assume that all promissory notes must include collateral. Although secured promissory notes exist, unsecured ones do not require collateral. The choice depends on the agreement between the lender and the borrower.

It's often thought that promissory notes are informal and don’t need to follow a specific format. However, to ensure legal enforceability in Massachusetts, certain key elements, such as the amount borrowed and the repayment schedule, must be clearly stated.

A final misconception is that promissory notes cannot be modified once signed. Both parties can agree to amend the terms if necessary, as long as the changes are documented and signed by both the lender and the borrower.

Dispelling these misconceptions is crucial for both lenders and borrowers to understand their rights and obligations fully. A well-informed approach can lead to smoother financial transactions and fewer disputes.

When preparing and utilizing the Massachusetts Promissory Note form, it's crucial to understand its significance and the necessary steps to ensure it's correctly completed and enforceable. Here are key takeaways to guide you through the process:

By keeping these key points in mind, users of the Massachusetts Promissory Note form can navigate the process more smoothly and ensure that their agreement is solid, fair, and legally binding.

Mass Rmv Bill of Sale - It's an essential document for private vehicle sales, where no dealership is involved in the transaction.

How to Make an Operating Agreement - An Operating Agreement is critical for clarifying verbal agreements between members, thus preventing future conflicts.

Massachusetts Transfer on Death Deed - For those concerned about maintaining privacy in their estate transactions, a Transfer-on-Death Deed is recorded publicly, but it keeps the property out of probate court.